如果结果不匹配,请

如果结果不匹配,请

更多“Financial statements are an ex…”相关的问题

更多“Financial statements are an ex…”相关的问题

W: First, financial statements are general-purpose statements. Secondly, the relationships between amounts on successive financial statements are not obvious without analysis. And thirdly, users of financial statements may be interested in seeing how well a company is performing.

Q: What are they talking about?

(17)

A.The methods of financial statements.

B.The necessity of careful analysis of financial statements

C.The relationship among financial statements.

D.The purpose of financial statements.

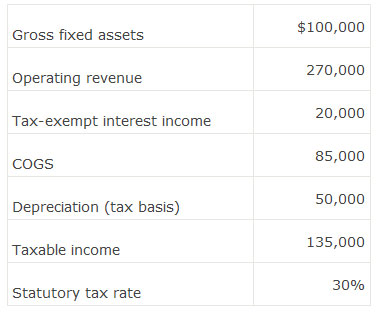

. Company Y’s fixed assets have a four-year useful life for financial purpose (which is double the useful life for tax purpose) and are depreciated using the straight-line method.

The effective tax rate for the company is closest to:

A.30.0%

B.26.7%

C.24.0%.

Two software companies that report their financial statements under U.S.GAAP (generally accepted accounting principles) are identical except as to how soon they judge a project to be technologically feasible.One firm does so very early in the development cycle while the other usually waits until just before the project is released to manufacturing.Compared to the company that judges technological feasibility early, the one that waits until closer to manufacturing will most likely report lower:

A.financial leverage.

B.total asset turnover.

C.cash flow from operations.

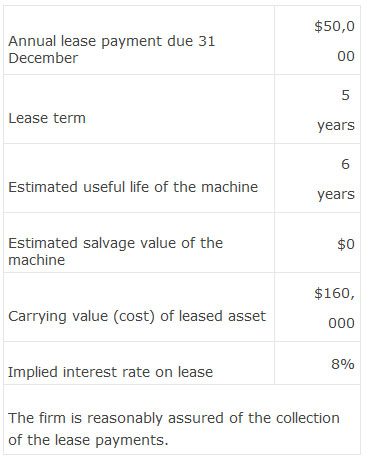

Which of the following best describes the classification of the lease on the company’s financial statements for 2008?

A.Operating lease.

B.Sales type lease.

C.Direct financing lease.

W: You are right. I find the comparison of financial statements between one year and the next, particularly helpful in understanding a company's performance.

Q: What are they talking about?

(16)

A.The performance of a company.

B.The financial statements.

C.The detailed information.

D.An extensive annual report.

A. An increase in tax expense and an increase to the debt-to-equity ratio.

B. An increase in tax expense and a decrease to the debt-to-equity ratio.

C. A decrease in tax expense and an increase to the debt-to-equity ratio.

A.The issuance of convertible bonds by a company results in a decrease in both its debt-to-equity and its interest coverage ratios.

B.The conversion of convertible bonds into common equity results in an increase in the company’s debt-to-equity ratio and an increase in the interest coverage ratio.

C.When there is a conversion of convertible debt into common equity, even if the market price exceeds the conversion price, no gain or loss may be reported on the financial statements.

A.straight-line.

B.declining balance.

C.units-of-production.

A.goodwill.

B.a trademark.

D.an intangible asset, research and development.

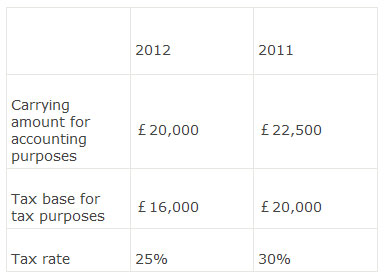

A company purchased equipment in 2011 for £25,000; the year-end values for accounting purposes and tax purposes are as follows:

Which of the following statements best describes the effect of the change in the tax rate on the company’s 2012 financial statements? The deferred tax liability:

A、Increased by £250

B、Decreased by £200

C、Decreased by £800